This was my biggest high-yield dividend shareholding - and I rated it a HOLD back in February. So, what has changed - do I think, perhaps, that the end of the world is coming?

|

| Source |

As I have been developing the blog, I have been putting the best of the posts together to document the DIY Income Investor approach in an e-book 'Building Wealth as a DIY Income Investor'.

As I have been developing the blog, I have been putting the best of the posts together to document the DIY Income Investor approach in an e-book 'Building Wealth as a DIY Income Investor'. |

| Source |

|

| Source |

|

| Source |

|

| Source |

|

| Source |

|

| Swings and roundabouts Source |

|

| Source |

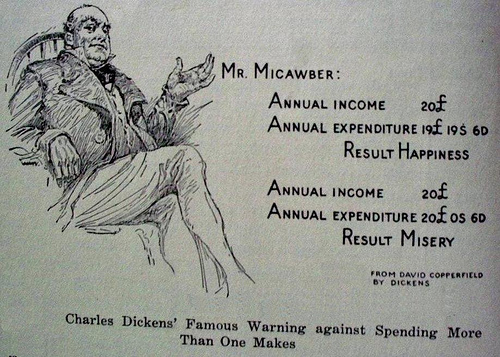

Managing your cash is a key skill. Debt is not allowed in the DIY Income Investor approach, so you need cash (i.e. rather than credit) for day-to-day expenses and for longer-term purchases or one-off costs, for which you will need an appropriately-sized 'emergency fund'.

Managing your cash is a key skill. Debt is not allowed in the DIY Income Investor approach, so you need cash (i.e. rather than credit) for day-to-day expenses and for longer-term purchases or one-off costs, for which you will need an appropriately-sized 'emergency fund'.  |

| Source |

It is satisfying when one of your investments performs well. But what should you do then? Just sit back and enjoy the warm glow?

It is satisfying when one of your investments performs well. But what should you do then? Just sit back and enjoy the warm glow? The search for yield in the UK is getting harder and harder. Perhaps this is a good thing, as it implies that market risks are seen as falling, as well being a result of governments around the world pumping money into governments stocks (and reducing benchmark 'risk-free' yields).

The search for yield in the UK is getting harder and harder. Perhaps this is a good thing, as it implies that market risks are seen as falling, as well being a result of governments around the world pumping money into governments stocks (and reducing benchmark 'risk-free' yields). |

| Source |

|

| Source |

| Source |

|

| Source |

|

| Source |

|

| Source |

|

| Source |

|

| Source |

|

| Some US Joneses? Source |

|

| Source |

The DIY Income Investor (and family) is going on holiday soon: 21 days of all-inclusive relaxation, away from the markets, with the portfolio on automatic pilot.

The DIY Income Investor (and family) is going on holiday soon: 21 days of all-inclusive relaxation, away from the markets, with the portfolio on automatic pilot. |

| A house built on sand Source |

|

| Source |

|

| The Morgan Stanley Bull Source |

|

| Source |

Share prices have been pushed remorselessly down during May, but as the UK Taxman has just given me some money, I am a cautious buyer.

Share prices have been pushed remorselessly down during May, but as the UK Taxman has just given me some money, I am a cautious buyer. |

| Source |

|

| Source |

|

| Source |

I've come over all Welsh - but am I chasing after Fool's Gold or have I really found a seam of gold.

I've come over all Welsh - but am I chasing after Fool's Gold or have I really found a seam of gold.  |

| Source |

Is it time to live a bit dangerously? That what the latest portfolio purchase would imply.

Is it time to live a bit dangerously? That what the latest portfolio purchase would imply. {kind=link}