Monday 31 January 2011

FTSE 100 Dividends in 2010 and 2011

'Pay Yourself First' - 'Regular Saver' Account (UK)

A practical approach to starting saving is to Pay Yourself First - before you pay your bills, before you buy food, before you do anything else, set aside a portion of your income to save. The first bill you pay each month should be to yourself. This habit, developed early, can help a person to build up their wealth.

High-Yield Shares - Dividend Report Cards

Avoid Bad Financial Advice - go DIY! (UK)

You really can't trust anyone else with your money - particularly if they stand to make money out of your decisions!

The Money Snowball and Compound Interest

As a DIY Income Investor, when you save and invest - if things go well - you will experience the Money Snowball - when your savings seem to take on a life of their own and multiply without you having to do much to help.

As a DIY Income Investor, when you save and invest - if things go well - you will experience the Money Snowball - when your savings seem to take on a life of their own and multiply without you having to do much to help. It is like a snowball rolling down a hill gradually increasing in size as well as increasing in speed. You are getting richer, faster.

Friday 28 January 2011

Balancing Asset Classes

How should you choose which asset class to invest in?

Gilts and Bonds (UK)

| No, not that kind of Bond... Source |

Government bonds/gilts are loans made to the government - and corporate bonds are loans made to businesses. Both classes of assets share similar features; the main difference is that gilts are a lot 'safer', as they are guaranteed by the issuing governmental authority (local or national).

Income from Shares (UK, US)

There are numerous academic studies showing the importance of dividends in stock market portfolio returns, and indeed showing that the shares prices of higher-yielding shares have tended to perform better.

Get Rich Slow

Hopefully the DIY Income Investor approach will resonate with you as a logical and sensible path to wealth over the coming years.

Thursday 27 January 2011

Get an Internet Broker (UK, US)

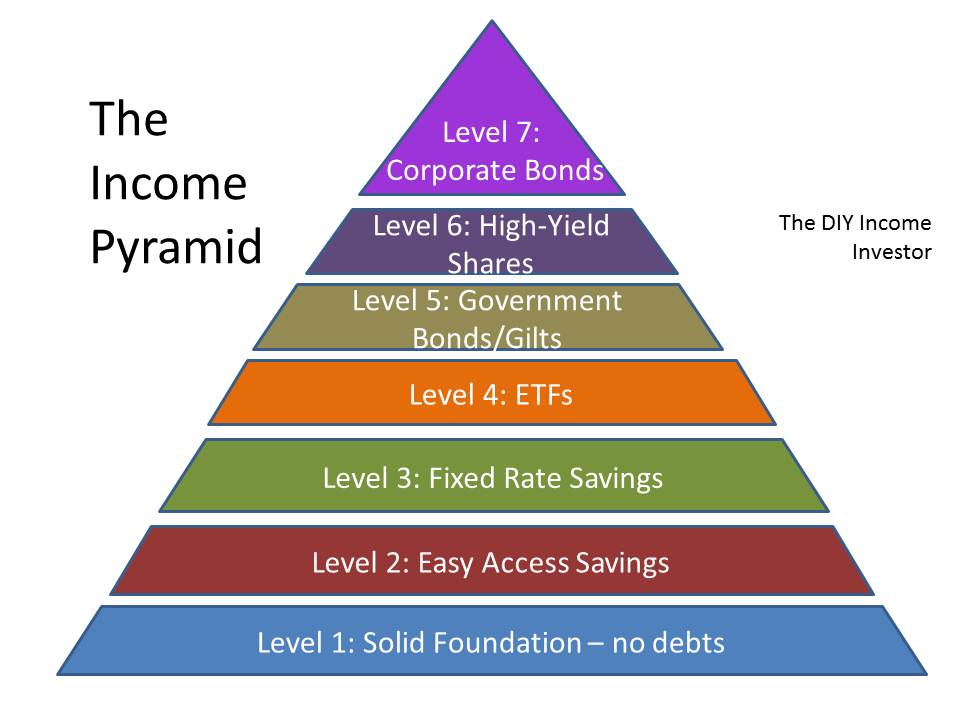

A core tool in becoming a DIY Income Investor is to manage your portfolio online. Once you have progressed to Level 4 on the Income Pyramid you will need an online Broker to access your local stockmarket.

Avoid Tax (legally!) (UK, US)

The 'Income Pyramid'

One way to understand the DIY Income Investor approach is to think of the different types of potential income as an 'Income Pyramid' - that is, layers of different sources of income, all built on a sound foundation and increasing in complexity (and hopefully in after-tax returns).

Why DIY?

Why should you Do It Yourself?

Why should you Do It Yourself?

If you have any doubts about the DIY approach, ask yourself the following questions:

- Who do I trust most?

- Who is going to act in my best interest?

- How does a Financial Advisor / Investment Broker / Insurance Salesman (etc.) make his money?

Welcome

Over the coming months (and hopefully years), I will be sharing a simple approach to building up and managing your savings and financial investments, with the primary aim of generating a growing income over time.

This approach will be mainly targeted at UK investors, although many of the underlying ideas should translate well to other locations, such as the US and elsewhere.

This approach will be mainly targeted at UK investors, although many of the underlying ideas should translate well to other locations, such as the US and elsewhere.

Subscribe to:

Posts (Atom)